Whether you have heard of the SECURE Act or not, it makes sense to understand the highlights of this recent legislation, which has some significant provisions affecting IRAs, retirement plans, 529 plans and more. The bill was officially signed into law on December 20, 2019 with most of the provisions going into effect as of January 1, 2020.

Major takeaways—The SECURE Act:

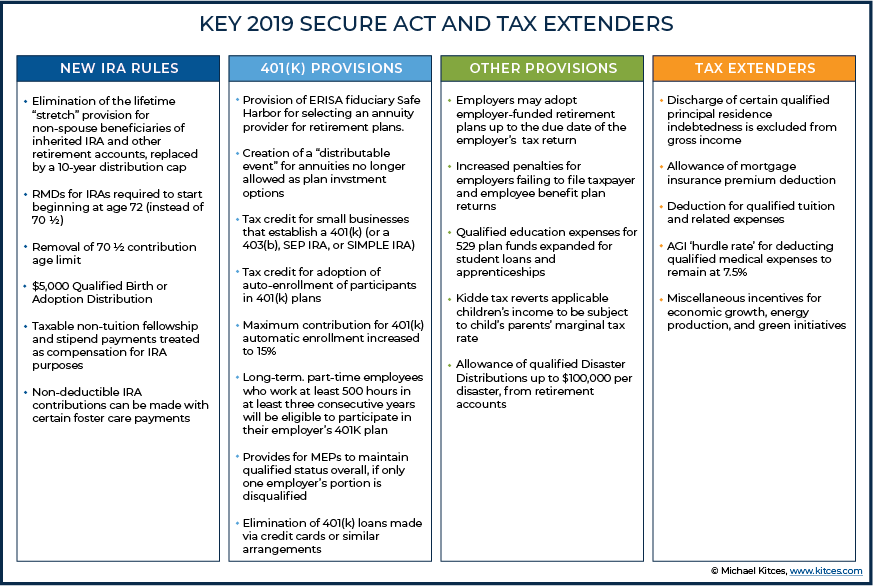

- Elimination of the “Stretch” IRA – replaced by the new 10-year rule

- Increases the required minimum distribution (RMD) age for retirement accounts to 72 (up from 70½).

- Repeals the maximum age for traditional IRA contributions, which is currently 70½.

- Allows parents to withdraw up to $10,000 from 529 plans to repay student loans.

Here is a summary of some of the key provisions of the SECURE Act:

Inherited IRA distributions generally must now be taken within 10 years:

Previously, if you inherited an IRA or 401(k), you could “stretch” your distributions over your life expectancy. Now, for IRAs inherited from original owners who have passed away on or after January 1, 2020, the new law requires many beneficiaries to withdraw assets from an inherited IRA or 401(k) plan within 10 years following the death of the account holder. Some exceptions to the 10-year rule include assets left to a surviving spouse, a minor child, a disabled or chronically ill beneficiary and beneficiaries who are less than 10 years younger than the original IRA owner or 401(k) participant.

Action step: If you have an IRA that you planned to leave to beneficiaries based on prior rules, consider working with your planner to review and evaluate your retirement and estate planning strategies. If you are a beneficiary of an inherited IRA or 401(k) and the original owner passed away prior to January 1, 2020, you don’t need to make any changes.

Required minimum distributions (RMDs) now begin at age 72:

Many Americans are working longer and will no longer be required to withdraw assets from IRAs and 401(k)s at age 70½.Individuals who turn 70½ in calendar year 2020 or later are not required to start taking their RMDs until age 72. If you turned age 70½ in 2019 and have already begun taking your RMD, you should generally continue to take your RMD.

Action step: If you are turning 70½ in 2020 and were planning on taking your RMD, you may want to work with your planner to reconsider your withdrawal plans.

You can make IRA contributions beyond age 70½: For those individuals who continue to work past their traditional retirement age, the SECURE Act allows you to continue to contribute to your traditional IRA past age 70½ as long as you are still working. That means the rules for traditional IRAs will align more closely with 401(k) plans and Roth IRAs.

Action step: Consider talking to your tax adviser or planner about the pros and cons of making IRA contributions for tax year 2020 and beyond.

529 funds can now be used to pay down student loan debt, up to $10,000:

In some cases, families have money remaining in their college savings plans after their student graduates. Now, they can use a 529 savings account to pay up to $10,000 in student debt over the course of the student’s lifetime. Under the new law, a 529 plan may also be used to pay for certain apprenticeship programs.

Action step: If your family’s 529 plans have money left over after you pay for college expenses, consider using the remaining money to help pay off student loans.

Other important provisions —The SECURE Act:

- Allows parents to take early withdrawals of up to $5,000 from a retirement plan without penalty within a year of a child’s birth or adoption.

- Makes it easier to provide a life annuity within a 401k.

- Allows long-term, part-time workers to participate in 401(k) plans.

- Offers more options for lifetime income strategies.

- Offers small-business owners tax credits for starting retirement plans and helps them facilitate the adoption of multiple employer plans (MEPs)

- Encourages retirement saving by raising the cap for auto enrollment contributions in employer-sponsored retirement plans from 10% of pay to 15%.

Major tax and retirement planning legislation is difficult to get passed in Congress and for that reason rarely occurs. But when it does, we need to make sure we understand the major provisions involved and how they may impact us and our families. We hope this summary helps to do just that.

Social Media